No Time for Pessimism about Electric Cars

The national push to adopt electric cars should be sustained until at least 2017, when a review of fed auto policies is scheduled.

A distinctive feature of U.S. energy and environmental policy is a strong push to commercialize electric vehicles (EVs). The push began in the 1990s with California’s Zero Emission Vehicle (ZEV) program, but in 2008 Congress took the push nationwide through the creation of a $7,500 consumer tax credit for qualified EVs. In 2009 the Obama administration transformed a presidential campaign pledge into an official national goal: putting one million plug-in electric vehicles on the road by 2015.

A variety of efforts has promoted commercialization of EVs. Through a joint rulemaking, the Department of Transportation and the Environmental Protection Agency are compelling automakers to surpass a fleet-wide average of 54 miles per gallon for new passenger cars and light trucks by model year 2025. Individual manufacturers, which are considered unlikely to meet the standards without EV offerings, are allowed to count each qualified EV as two vehicles instead of one in near-term compliance calculations.

The U.S. Department of Energy (DOE) is actively funding research, development, and demonstration programs to improve EV-related systems. Loan guarantees and grants are also being used to support the production of battery packs, electric drive-trains, chargers, and the start-up of new plug-in vehicle assembly plants. The absence of a viable business model has slowed the growth of recharging infrastructure, but governments and companies are subsidizing a growing number of public recharging stations in key urban locations and along some major interstate highways. Some states and cities have gone further by offering EV owners additional cash incentives, HOV-lane access, and low-cost city parking.

Private industry has responded to the national EV agenda. Automakers are offering a growing number of plug-in EV models (three in 2010; seventeen in 2014), some that are fueled entirely by electricity (battery-operated electric vehicles, or BEVs) and others that are fueled partly by electricity and partly by a back-up gasoline engine (plug-in hybrids, or PHEVs). Coalitions of automakers, car dealers, electric utilities, and local governments are working together in some cities to make it easy for consumers to purchase or lease an EV, to access recharging infrastructure at home, in their office or in their community, and to obtain proper service of their vehicle when problems occur. Government and corporate fleet purchasers are considering EVs while cities as diverse as Indianapolis and San Diego are looking into EV sharing programs for daily vehicle use. Among city planners and utilities, EVs are now seen as playing a central role in “smart” transportation and grid systems.

The recent push for EVs is hardly the market-oriented approach to innovation that would have thrilled Milton Friedman. It resembles somewhat the bold industrial policies in the post-World War II era that achieved some significant successes in South Korea, Japan, and China. Although the U.S. is a market-oriented economy, it is difficult to imagine that the U.S. successes in aerospace, information technology, nuclear power, or even shale gas would have occurred without a supportive hand from government. In this article, we make a pragmatic case for stability in federal EV policies until 2017, when a large body of real-world experience will have been generated and when a midterm review of federal auto policies is scheduled.

Laurence Gartel and Tesla Motors

Digital artist Laurence Gartel collaborated with Tesla Motors to transform the electric Tesla Roadster into a work of art by wrapping the car’s body panels in bold colorful vinyl designed by the artist. The Roadster was displayed and toured around Miami Beach during Miami’s annual Art Basel festival in 2010.

Gartel, an artist who has experimented with digital art since the 1970s, was a logical collaborator with Tesla given his creative uses of technology. He graduated from the School of Visual Arts, New York, in 1977, and has pursued a graphic style of digital art ever since. His experiments with computers, starting in 1975, involved the use of some of the earliest special effects synthesizers and early video paint programs. Since then, his work has been exhibited at the Museum of Modern Art; Long Beach Museum of Art; Princeton University Art Museum; MoMA PS 1, New York City; and the Norton Museum of Art, West Palm Beach, Florida. His work is in the collections of the Smithsonian Institution’s National Museum of American History and the Bibliotheque Nationale, Paris.

Image courtesy of the artist.

Governmental interest in EVs

The federal government’s interest in electric transportation technology is rooted in two key advantages that EVs have over the gasoline- or diesel-powered internal combustion engine. Since the advantages are backed by an extensive literature, we summarize them only briefly here.

First, electrification of transport enhances U.S. energy security by replacing dependence on petroleum with a flexible mixture of electricity sources that can be generated within the United States (e.g. natural gas, coal, nuclear power, and renewables). The U.S. is making rapid progress as an oil producer, which enhances security, but electrification can further advance energy security by curbing the nation’s high rate of consumption in the world oil market. The result: less global dependence on energy from OPEC producers, unstable regimes in the Middle East, and Russia.

Second, electrification of transport is more sustainable on a life-cycle basis because it causes a net reduction in local air pollution and greenhouse gas emissions, an advantage that is expected to grow over time as the U.S. electricity mix shifts toward more climate-friendly sources such as gas, nuclear, and renewables. Contrary to popular belief, an electric car that is powered by coal-fired electricity is still modestly cleaner from a greenhouse gas perspective than a typical gasoline-powered car. And EVs are much cleaner if the coal plant is equipped with modern pollution controls for localized pollutants and if carbon capture and storage (CCS) technology is applied to reduce carbon dioxide emissions. Since the EPA is already moving to require CCS and other environmental controls on coal-fired power plants, the environmental case for plug-in vehicles will only become stronger over time.

Although the national push to commercialize EVs is less than six years old, there have been widespread claims in the mainstream press, on drive-time radio, and on the Internet that the EV is a commercial failure. Some prominent commentators, including Charles Krauthammer, have suggested that the governmental push for EVs should be reconsidered.

It is true that many mainstream car buyers are unfamiliar with EVs and are not currently inclined to consider them for their next vehicle purchase. Sales of the impressive (and pricy) Tesla sports car (Model S) have been better than the industry expected, but ambitious early sales goals for the Nissan Leaf (a BEV) and the Chevrolet Volt (a PHEV) have not been met. General Electric Corporation backed off of an original pledge to purchase 25,000 EVs. Several companies with commercial stakes in batteries, EVs, or chargers have gone bankrupt, despite assistance from the federal government.

“Early adopters” of plug-in vehicles are generally quite enthusiastic about their experiences, but mainstream car buyers remain hesitant. There is much skepticism in the industry about whether EVs will penetrate the mainstream new-vehicle market or simply serve as “compliance cars” for California regulators or become niche products for taxi and urban delivery fleets.

One of the disadvantages of EVs is that they are currently more costly to produce than comparably sized gasoline and diesel powered vehicles. The cost premium today is about $10,000-$15,000 per vehicle, primarily due to the high price of lithium ion battery packs. The cost disadvantage has been declining over time due to cost-saving innovations in battery-pack design and production techniques but there is a disagreement among experts about how much and how fast production costs will decline in the future.

On the favorable side of the affordability equation, EVs have a large advantage in operating costs: electricity is about 65% cheaper than gasoline on an energy-equivalent basis, and most analysts project that the price of gasoline in the United States will rise more rapidly over time than the price of electricity. Additionally, repair and maintenance costs are projected to be significantly smaller for plug-in vehicles than gasoline vehicles. When all of the private financial factors are taken into account, the total cost of ownership throughout the lifetime of the EV is comparable—or even lower—than a gasoline vehicle, and that advantage can be expected to enlarge as EV technology matures.

Trends in EV sales

Despite the financial, environmental, and security advantages of the EV, early sales have not matched initial hopes. Nissan and General Motors led the high-volume manufacturers with EV offerings but have had difficulty generating sales, even though auto sales in the United States were steadily improving from 2010 through 2013, the period when the first EVs were offered. In 2013 EVs accounted for only about 0.2% of the 16 million new passenger vehicles sold in the U.S.

Nissan-Renault has been a leader. At the 2007 Tokyo Motor Show, Nissan shocked the industry with a plan to leapfrog the gasoline-electric hybrid with a new mass-market BEV, called the Fluence in France and the Leaf in the U.S. Nissan’s business plan called for EV sales of 100,000 per year in the U.S. by 2012, and Nissan was awarded a $1.6 billion loan guarantee by DOE to build a new facility in Smyrna, Tennessee to produce batteries and assemble EVs. The company had plans to sell 1.5 million EVs on a global basis by 2016 but, as of late 2013, had sold only 120,000 and acknowledged that it will fall short of its 2016 global goal by more than 1 million vehicles.

General Motors was more cautious than Nissan, planning production in the US of 10,000 Volts in 2011 and 60,000 in 2012. However, neither target was met. GM did “re-launch” the Volt in early 2012 after addressing a fire-safety concern, obtaining HOV-lane access in California for Volt owners, cutting the base price, and offering a generous leasing arrangement of $350 per month for 36 months of use. Volt sales rose from 7,700 in 2011 to 23,461 in 2012 and 23,094 in 2013.

The most recent full-year U.S. sales data (2013) reveal that the Volt is now the top-selling plug-in vehicle in the U.S., followed by the Leaf (22,610), the Tesla Model S (18,000), and the Toyota Prius Plug-In (12,088). In the first six months of 2014, EV sales are up 33% over 2013, led by the Nissan Leaf and an impressive start from the Ford Fusion Energi PHEV. Although the sales at Tesla have slowed a bit, the company has announced plans for a new $5 billion plant in the southwest of the U.S. to produce up to 500,000 vehicles for distribution worldwide.

President Obama, in 2009 and again in his January 2011 State of the Union address, set the ambitious goal of putting one million plug-in vehicles on the road by 2015. Two years after the address, DOE and the administration dropped the national 2015 goal, recognizing that it was overly ambitious and would take longer to achieve. But does this refinement of a federal goal really prove that EVs are a commercial failure? We argue that it does not, pointing to two primary lines of evidence: a historical comparison of EV sales with conventional hybrid sales; and a cross-country comparison of U.S. EV sales with German EV sales.

Comparison with the conventional hybrid

A conventional hybrid, defined as a gasoline-electric vehicle such as the Toyota Prius, is different from a plug-in vehicle. Hybrids vary in their design, but they generally recharge their batteries during the process of braking (“regenerative braking”) or, if the brakes are not in use during highway cruising, from the power of the gasoline engine. Thus, a conventional hybrid cannot be plugged in for charging and does not draw electricity from the grid.

Cars with hybrid engines are also more expensive to produce than gasoline cars, primarily because they have two propulsion systems. For a comparably-sized vehicle, the full hybrid costs $4,000 to $7,500 more to produce than a gasoline version. But the hybrid buyer can expect 30% better fuel economy and fewer maintenance and repair costs than a gasoline-only engine. According to recent life-cycle and cost-benefit analyses, conventional hybrids compare favorably to the current generation of EVs.

Toyota is currently the top seller of hybrids, offering 22 models globally that feature the gasoline-electric combination. To date, the Prius has sold over 3 million vehicles worldwide, and has recently expanded to an entire family of models. In 2013, U.S. sales of the Prius were 234,228, of which 30% were registered in the State of California, where the Prius was the top-selling vehicle line in both 2012 and 2013.

The success of the Prius did not occur immediately after introduction. Toyota and Honda built on more than a decade of engineering research funded by DOE and industry. Honda was actually the first company to offer a conventional hybrid in the U.S.—the Insight Hybrid in 1999—but Toyota soon followed in 2000 with the more successful Prius. Ford followed with the Escape Hybrid SUV. The experience with conventional hybrids underscores the long lead times in the auto industry, the multiyear process of commercialization, and the conservative nature of the mainstream U.S. car purchaser.

Fifteen years ago, critics of conventional hybrids argued that the fuel savings would not be enough to justify the cost premium of two propulsion systems, that the batteries would deteriorate rapidly and require expensive replacement, that resale values for hybrids would be discounted, that the batteries might overheat and create safety problems, and that hybrids were practical only for small, light-weight cars. “Early adopters” of the Prius, which carried a hefty price premium for a small car, were often wealthy, highly educated buyers who were attracted to the latest technology or wanted to make a pro-environment statement with their purchase. The process of expanding hybrid sales from early adopters to mainstream consumers took many years to occur, and that process continues today, fifteen years later.

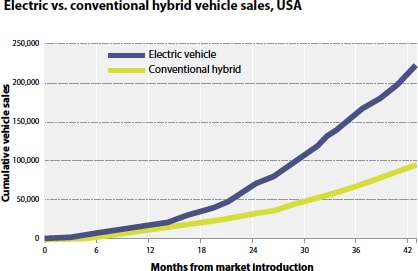

When the EV and the conventional hybrid are compared according to the pace of market penetration in the United States, the EV appears to be more successful (so far). Figure 1 illustrates this comparison by plotting the cumulative number of vehicles sold—conventional hybrids versus EVs—during the first 43 months of market introduction. At month 25, EV sales were about double the number of hybrid sales; at month 40 the ratio of cumulative EV sales to cumulative hybrid sales was about 2.2. The overall size of the new passenger-vehicle market was roughly equal in the two time periods.

When comparing the penetration rates of hybrids and EVs, it is useful to highlight some of the differences in the technologies, policies, and economic environments. The plug-in aspect of the EV calls for a much larger change in the routine behavior of motorists (e.g., nighttime and community charging) than does the conventional hybrid. The early installations of 220-volt home charging stations, which reduce recharging time from 12-18 hours to 3-4 hours, were overly expensive, time-consuming to set up with proper permits, and an irritation to early adopters of EVs. Moreover, the EV owner is more dependent on the decisions of other actors (e.g., whether employers or shopping malls supply charging stations and whether the local utility offers low electricity rates for nighttime charging) than is the hybrid owner.

The success of the conventional hybrid helped EVs get started by creating an identifiable population of potential early adopters that marketers of the EV have exploited. Now, one of the significant predictors of EV ownership is prior ownership of a conventional hybrid. Some of the early EV owners immediately gained HOV access in California, but Prius owners were not granted HOV lane access until 2004, several years after market introduction. California phased out HOV access for hybrids from 2007 to 2011 and now awards the privilege to qualified EV owners.

From a financial perspective, the purchase of the conventional hybrid and EV were not equally subsidized by the government. EV purchasers were enticed by a $7,500 federal tax credit; the tax deduction—and later credit—for conventional hybrid ownership was much smaller, at less than $3,200. Some states (e.g., California and Colorado) supplemented the $7,500 federal tax credit with $1,000 to $2,500 credits (or rebates) of their own for qualified EVs; few conventional hybrid purchasers were provided a state-level purchase incentive. Nominal fuel prices were around $2 per gallon but rising rapidly in 2000-2003, the period when the hybrid was introduced to the U.S. market; fuel prices were volatile and in the $3-$4 per gallon range from 2010-2013 when EVs were initially offered. The roughly $2,000 cost of a Level 2 (220-volt) home recharging station (equipment plus labor for installation) was for several years subsidized by some employers, utilities, government grants, or tax credits. Overall, financial inducements to purchase an EV from 2010 to 2013 were stronger than the inducements for a conventional hybrid from 2000 to 2003, possibly helping explain why the take-up of EVs has been faster.

Comparison with Germany

Another way to assess the success of EV sales in the United States since 2010 is to compare it to another country where EV policies are different. Germany is an interesting comparator because it is a prosperous country with a strong “pro-environment” tradition, a large and competitive car industry, and relatively high fuel prices of $6-$8 per gallon due to taxation. Electricity prices are also much higher in Germany than the U.S. due to an aggressive renewables policy.

Like President Barack Obama, German Prime Minister Angela Merkel has set a goal of putting one million plug-in vehicles on the road, but the target date in Germany is 2020 rather than 2015. Germany has also made a large public investment in R&D to enhance battery technology and a more modest investment in community-based demonstrations of EV technology and recharging infrastructure.

On the other hand, Germany has decided against instituting a large consumer tax credit similar to the €10,000 “superbonus” for EVs that is available in France. Small breaks for EV purchasers in Germany are offered on vehicle sales taxes and registration fees. Nothing equivalent to HOV-lane access is offered to German EV users yet. Germany also offers few subsidies for production of batteries and electric drivetrains and no loan guarantees for new plants to assemble EVs.

Since the German car manufacturers are leaders in the diesel engine market, the incentive for German companies to explore radical alternatives to the internal combustion engine may be tempered. Also, German engineers appear to be more confident in the long-term promise of the hydrogen fuel cell than in cars powered by lithium ion battery packs. Even the conventional hybrid engine has been slow to penetrate the German market, though there is some recent interest in diesel-electric hybrid technology. Daimler and Volkswagen have recently begun to offer EVs in small volumes but the advanced EV technology in BMW’s “i” line is particularly impressive.

FIGURE 1

Another key difference between Germany and the U.S. is that Germany has no regulation similar to California’s Zero Emission Vehicle (ZEV) program. The latest version of the ZEV mandate requires each high-volume manufacturer doing business in California to offer at least 15% of their vehicles as EVs or fuel cells by 2025. Some other states (including New York), which account for almost a quarter of the auto market, have joined the ZEV program. The ZEV program is a key driver of EV offerings in the US. In fact, some global vehicle manufacturers have stated publicly that, were it not for the ZEV program, they might not be offering plug-in vehicles to consumers. Since the EU’s policies are less generous to EVs, some big global manufacturers are focusing their EV marketing on the West Coast of the U.S. and giving less emphasis to Europe.

Overall, from 2010 to 2013 Germany has experienced less than half of the market-share growth in EV sales than has occurred in the U.S. The difference is consistent with the view that the policy push in the U.S. has made a difference. The countries in Europe where EVs are spreading rapidly (Norway and the Netherlands) have enacted large financial incentives for consumers coupled with coordinated municipal and utility policies that favor EV purchase and use.

Addressing barriers to adoption of EVs

The EV is not a static technology but a rapidly evolving technological system that links cars with utilities and the electrical grid. Automakers and utilities are addressing many of the barriers to more widespread market diffusion, guided by the reactions of early adopters.

Acquisition cost. The price premium for an EV is declining due to savings in production costs and price competition within the industry. Starting in February 2013, Nissan dropped the base price of the Leaf from $35,200 to $28,800 with only modest decrements to base features (e.g., loss of the telematics system). Ford and General Motors responded by dropping the prices of the Focus Electric and Volt by $4,000 and $5,000, respectively. Toyota chipped in with a $4,620 price cut on the plug-in version of the Toyota Prius (now priced under $30,000), but it is eligible for only a $2,500 federal tax credit. And industry analysts report that the transaction prices for EVs are running even lower than the diminished list prices, in part due to dealer incentives and attractive financing deals.

Dealers now emphasize affordable leasing arrangements, with a majority of EVs in the U.S. acquired under leasing deals. Leasing allays consumer concerns that the batteries may not hold up to wear and tear, that resale values of EVs may plummet after purchase (a legitimate concern), and that the next generation of EVs may be vastly improved compared to current offerings. Leasing deals for under $200 per month are available for the Chevy Spark EV, the Fiat 500e, the Leaf, Daimler’s Smart For Two EV; lease rates for the Honda Fit EV, the Volt and the Ford Focus EV are between $200 and $300 per month. Some car dealers offer better deals than the nationwide leasing plans provided by vehicle manufacturers.

Driving range. Consumer concerns about limited driving range—80-100 miles for most EVs, though the Tesla achieves 200-300 miles per charge—are being addressed in a variety of ways. PHEVs typically have maximum driving ranges that are equal to (or better than) a comparable gasoline car, and a growing body of evidence suggests that PHEVs may attract more retail customers than BEVs. For consumers interested in BEVs, some dealers are also offering free short-term use of gasoline vehicles for long trips when the BEV has insufficient range. The upscale BMW i3 EV is offered with an optional gasoline engine for $3,850 that replenishes the battery as it runs low; the effective driving range of the i3 is thus extended from 80-100 miles to 160-180 miles.

Recharging time. Some consumers believe that the 3-4 hour recharging time with a Level 2 charger is too long. Use of super-fast Level 3 chargers can accomplish an 80% charge in about 30 minutes, although inappropriate use of Level 3 chargers can potentially damage the battery. In the crucial West Coast market, where consumer interest in EVs is the highest, Nissan is subsidizing dealers to make Level 3 chargers available for Leaf owners. BMW is also offering an affordable Level 3 charger. State agencies in California, Oregon, and Washington are expanding the number of Level 2 and Level 3 chargers available along interstate highways, especially Interstate 5, which runs from the Canadian to the Mexican borders.

As of 2013, a total of 6,500 Level 2 and 155 Level 3 charging stations were available to the U.S. public. Some station owners require users to be a member of a paid subscription plan. Tesla has installed 103 proprietary “superchargers” for its Model S that allow drivers to travel across the country or up and down both coasts with only modest recharging times. America’s recharging infrastructure is tiny compared to the 170,000 gasoline stations, but charging opportunities are concentrated in areas where EVs are more prevalent, such as southern California, San Francisco, Seattle, Dallas-Fort Worth, Houston, Phoenix, Chicago, Atlanta, Nashville, Chattanooga, and Knoxville.

Advanced battery and grid systems. R&D efforts to find improved battery systems have intensified. DOE recently set a goal of reducing the costs of battery packs and electric drive systems by 75% by 2022, with an associated 50% reduction in the current size and weight of battery packs. Whether DOE’s goals are realistic is questionable. Toyota’s engineers believe that by 2025 improved solid-state and lithium air batteries will replace lithium ion batteries for EV applications. The result will be a three- to five-fold rise in power at a significantly lower cost of production due to use of fewer expensive rare earths. Lithium-sulfur batteries may also deliver more miles per charge and better longevity than lithium ion batteries.

Researchers are also exploring demand side management of the electrical grid with “vehicle-to-grid” (V2G) technology. This innovation could enable electric car owners to make money by storing power in their vehicles for later use by utilities on the grid. It might cost an extra $1,500 to fit a V2G-enabled battery and charging system to a vehicle but the owner might recoup $3,000 per year from a load-balancing contract with the electric utility. It is costly for utilities to add storage capacity; the motorist already needs the battery for times when the vehicle is in use, so a V2G contract might allow for optimal use of the battery.

Low-price electricity and EV sharing. Utilities and state regulators are also experimenting with innovative charging schemes that will favor EV owners who charge their vehicles at times when electricity demand is low. Mandatory time-of-use pricing has triggered adverse public reactions but utilities are making progress with more modest, incentive-based pricing schemes that favor nighttime and weekend charging. Atlanta is rapidly becoming the EV capital of the southern United States, in part because Georgia’s utilities offer ultra-low electricity prices to EV owners.

A French-based company has launched electric-car sharing programs in Paris and Indianapolis. Modeled after bicycle sharing, consumers can rent an e-car for several hours or an entire day if they need a vehicle for multiple short trips in the city. The vehicle can be accessed with your credit card and returned at any of multiple points in the city. The commercial success of EV sharing is not yet demonstrated, but sharing schemes may play an important role in raising public awareness of the advancing technology.

The EV’s competitors

The future of the EV would be easier to forecast if the only competitor were the current version of the gasoline engine. History suggests, however, that unexpected competitors can emerge that change the direction of consumer purchases.

The EV is certainly not a new idea. In the 1920s, the United States was the largest user of electric cars in the world, and more electric than gasoline-powered cars were sold. Actually, steam-powered cars were among the most popular offerings in that era.

EVs and steam-powered cars lost out to the internal combustion engine for a variety of reasons. Discovery of vast oil supplies made gasoline more affordable. Mass production techniques championed by Henry Ford dropped the price of a gasoline car more rapidly than the price of an electric car. Public investments in new highways connected cities, increased consumer demand for vehicles with long driving range, and therefore reduced the relative appeal of range-limited electric cars, whose value was highest for short trips inside cities. And car engineers devised more convenient ways to start a gasoline-powered vehicle, which caused them to be more appealing to female as well as male drivers. By the 1930s, the electric car lost its place in the market and did not return for many decades.

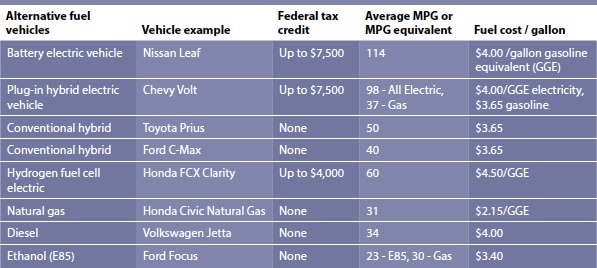

Looking to the future, it is apparent that EVs will confront intensified competition in the global automotive market. The vehicles described in Table 1 are simply an illustration of the competitive environment.

Vehicle manufacturers are already marketing cleaner gasoline engines (e.g., Ford’s “EcoBoost” engines with turbochargers and direct-fuel injection) that raise fuel economy significantly at a price premium that is much less than the price premium for a conventional hybrid or EV. Clean diesel-powered cars, which have already captured 50% of the new-car market in Europe, are beginning to penetrate the U.S. market for cars and pick-up trucks. Toyota argues that an unforeseen breakthrough in battery technology will be required to enable a plug-in vehicle to match the improving cost-effectiveness of a conventional hybrid.

Meanwhile, the significant reduction in natural gas prices due to the North American shale-gas revolution is causing some automakers to offer vehicles that can run on compressed natural gas or gasoline. Proponents of biofuels are also exploring alternatives to corn-based ethanol that can meet environmental goals at a lower cost than an EV. Making ethanol from natural gas is one of the options under consideration. And some automakers believe that hydrogen fuel cells are the most attractive long-term solution, as the cost of producing fuel cell vehicles is declining rapidly.

TABLE 1

As attractive as some of the EV’s competitors may be, it is unlikely that regulators in California and other states will lose interest in EVs. (In theory, the ZEV mandate also gives manufacturers credit for cars with hydrogen fuel cells but the refueling infrastructure for hydrogen is developing even more slowly than it is for EVs). A coalition of eight states, including California, recently signed a Memorandum of Understanding aimed at putting 3.3 million EVs on the road by 2025. The states, which account for 23% of the national passenger vehicle market, have agreed to extend California’s ZEV mandate, hopefully in ways that will allow for compliance flexibility as to exactly where EVs are sold.

ZEV requirements do not necessarily reduce pollution or oil consumption in the near term, since they are not coordinated with national mileage and pollution caps. Thus, when more ZEVs are sold in California and other ZEV states, it frees automakers to sell more fuel-inefficient and polluting vehicles in non-ZEV states. Without better coordination between individual states and the federal policies, the laudable goals of the ZEV mandate could be frustrated.

All things considered, America’s push toward transport electrification is off to a modestly successful start, even though some of the early goals for market penetration were overly ambitious. Automakers were certainly losing money on their early EV models but that was true of conventional hybrids as well. The second generation of EVs now arriving in showrooms is likely to be more attractive to consumers, since they have been refined based on the experiences of early adopters. And as more recharging infrastructure is added, cautious consumers with “range anxiety” may become more likely to consider a BEV, or at least a PHEV.

Vehicle manufacturers and dealers are also beginning to focus on how to market the unique performance characteristics of an EV. Instead of touting primarily fuel savings or environmental virtue, marketers are beginning to echo a common sentiment of early adopters: EVs are enjoyable to drive because, with their relatively high torque and quiet yet powerful acceleration, they are a unique driving experience.

Now is not the right time to redo national EV policies. EVs and their charging infrastructure have not been available long enough to draw definitive conclusions. Vehicle manufacturers, suppliers, utilities, and local governments have made large EV investments with an understanding that federal auto-related policies will be stable until 2017, when a national mid-term policy review is scheduled.

It is not too early to frame some of the key issues that will need to be considered between now and 2017. First, are adequate public R&D investments being made in the behavioral as well as technological aspects of transport electrification? We believe that DOE needs to reaffirm the commitment to better battery technology while giving more priority to understanding the behavioral obstacles to all forms of green vehicles. Second, we question whether national policy should continue a primary focus on EVs. It may be advisable to stimulate a more diverse array of green vehicle technologies, including cars fueled by natural gas, hydrogen, advanced ethanol, and clean diesel fuel. Third, federal mileage and carbon standards may need to be refined to ensure cost-effectiveness and to provide a level playing field for the different propulsion systems. Fourth, highway-funding schemes need to shift from gasoline taxes to mileage-based road user fees in order to ensure that adequate funds are raised for road repairs and that owners of green vehicles pay their fair share. Fifth, California’s policies need to be better coordinated with federal policies in ways that accomplish environmental and security objectives and allow vehicle manufacturers some sensible compliance flexibility. Finally, on an international basis, policy makers in the European Union, Japan, Korea, China, California and the United States should work together to accomplish more regulatory cooperation in this field, since manufacturers of batteries, chargers, and vehicles are moving toward global platforms that can efficiently provide affordable technology to consumers around the world.

Coming to a policy consensus in 2017 will not be easy. In light of the fast pace of change and the many unresolved issues, we recommend that universities and think tanks begin to sponsor conferences, workshops, and white papers on these and related policy issues, with the goal of analyzing the available information to create well-grounded recommendations for action come 2017.

John D. Graham (grahamjd@indiana.edu) is dean, Joshua Cisney is a graduate student, Sanya Carley is an associate professor, and John Rupp is a senior research scientist at the School of Public and Environmental Affairs at Indiana University.