Congress Has Ruined America’s Beaches

1968’s National Flood Insurance Program set off a disastrous and expensive 50-year building boom on the coasts. Why can’t we undo it?

On March 5, 1962, the Ash Wednesday Storm, an enormous nor’easter, began battering the East Coast, from southern New England to northern Florida. People also called it “the five high storm” because it chewed away at the coast through five unusually high tides. By the time it faded, it had killed more than three dozen people, injured hundreds more, and left an estimated $200 million in coastal property damage (about $1.8 billion today).

It would be the coast’s “storm of record” for decades.

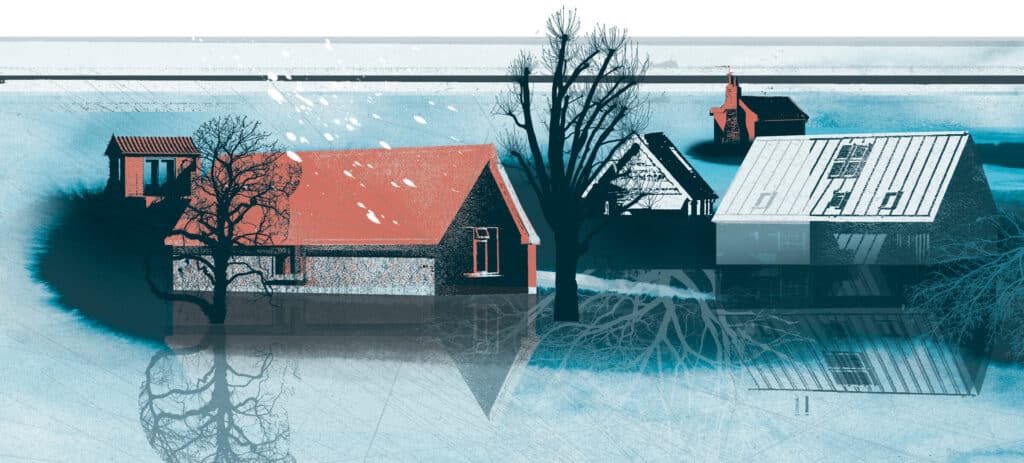

Today the nation faces a shattered coastal landscape and continuing bills for spending to prop up all of this beachfront building.

Two important developments rose out of the storm’s wreckage: intensified study of the geological processes that shape the coast, and interest in policies to reduce the need for disaster aid after coastal storms. Soon geologists began to measure the environmental costs of building on the coast, while policy-makers worked to make such building affordable—and more and more widespread. Just as geologists were realizing that beach development damaged beaches, the government began working to support development that in turn generated new demands for still more infrastructure on the beach. As a result, today the nation faces a shattered coastal landscape and continuing bills for spending to prop up all of this beachfront building.

How did we get into this mess? And how can we get out of it? Though I have spent decades reporting on the coast and its problems, I cannot say I have the answer. But I have some thoughts.

How subsidized insurance transformed the beach

In 1962, coastal research was a relatively new field—in part because the surf zone, where storm waves move sand most forcefully to reshape the beach—is notoriously unfriendly to instruments and researchers alike. Planning the amphibious landings of World War II had given the field a boost, but two decades later much was unknown about the forces shaping the coast.

Almost immediately after the Ash Wednesday Storm, geologists noticed something important: natural beaches—beaches that had not been built on—recovered quickly, starting within days of the storm’s passage. In contrast, built-up beaches recovered slowly, or hardly at all. This short-term observation has proved to be robust. Geologists have confirmed that most beaches can survive indefinitely, shifting with the seasons, even migrating inland as sea level rises—if they are not pinned down by development.

Meanwhile, policy-makers in Congress, disturbed by the cost of disaster relief after the storm, began work on a program they hoped would greatly reduce future bills. This work culminated in the National Flood Insurance Program, which since 1968 has offered low-cost insurance to property owners in coastal or riverine flood zones.

Backers of the program asserted that requirements to purchase the insurance, coupled with the program’s building code requirements, would discourage development in flood hazard zones. But far from discouraging risky coastal construction, the low-cost insurance supercharged it. Once property owners could obtain property insurance, federally insured banks were allowed to issue them mortgages. The result was a building boom that continues today. And even though coverage is limited to $250,000 for the structure and $150,000 for contents—far less than the value of many coastal homes—the program works, in effect, like a $400,000 deductible, making additional, private insurance far cheaper.

Natural beaches—beaches that had not been built on—recovered quickly, starting within days of the storm’s passage. In contrast, built-up beaches recovered slowly, or hardly at all.

Premiums from the insurance program were supposed to cover policy payouts, but they were set too low—typically only a few hundred dollars a year for insurance that would otherwise have cost thousands. Initially, and sporadically, it ran in the black, but claims after hurricanes routinely sent the program to the US Treasury for loans. Hurricanes Hugo, Andrew, Katrina, and Sandy shoved the program into permanent insolvency. Meanwhile, as the quantity of building on risky land grew, and the values of those properties also increased, the potential liability of the program has climbed to $1.3 trillion. As a result, the program has achieved a seemingly permanent place on the Government Accountability Office’s biennial High Risk List of programs in need of broad reform.

Because the program shifted the financial risks of building on the coast away from property owners and onto the taxpayers, it encouraged more people to live on the beach. Over the years, these people became a constituency pressing the government for new taxpayer support for their precarious communities.

Trying to nail sand to the beach

The coastal landscape is constantly in motion, changing shape on time scales ranging from hours to millennia. Until the last 50 years or so, few people chose to build on these shifting beaches with their dangerous storms. The Wampanoag people of southern New England, where I live now, may have invented the clambake, but when summer ended they would make their way to safety inland. Early settlers from Europe made their homes in sheltered spots inland from the harsh outer beaches, and Gilded Age plutocrats perched mansions high above the sand on the bedrock of Newport and Bar Harbor. Sure, there were small, cheap, parcels of beach where people built cabins so they could fish or paint landscapes, but these “camps” were modest affairs. If a storm washed them away, they were cheap to replace.

The flood insurance program changed all that, replacing flimsy shacks with a sprawl of condos and showcase homes. And when subsidized flood insurance took away the risks of owning beachfront property, the fishers and painters gave way to people who invested in more substantial homes, and who soon sought ways to stabilize their inherently unstable landscape.

The result has been decades of efforts to engineer solutions to protect endangered property, maintain sand on beaches, and even raise buildings out of harm’s way.

The oldest way to stabilize an inherently unstable coastal landscape is to armor it. Once the building boom started, armor, including sheet pilings, boulder riprap, and massive engineered concrete structures, became common on American beaches. This armor is unsightly, but the worst thing about it is its effect on the beach, especially what is called the intertidal zone: the wet beach between the sea at low tide and the shore at high tide. In most of the United States, the right to use this narrow strip of wet sand is enshrined in common law, dating to sixth century Rome’s Code of Justinian, as held in public trust. As such, this landscape is incapable of alienation—that is, in theory, it cannot legally be taken away. However, if you put a stationary barrier on an eroding beach, seawater will eventually rise to meet it, leaving the beach—including the intertidal zone—under water. Today this phenomenon can be seen from Charlestown, Rhode Island, to Galveston, Texas, to Malibu, California. In effect, we have traded away beaches for buildings.

To protect construction, salt marshes have become another target for walls and armor. The United States is estimated to have lost at least half of its coastal wetlands since colonial times, and we are on track to lose far more.

By now, people hardly notice riprap and concrete at the seashore. Generation by generation, people have accepted as normal an increasingly debased landscape—a phenomenon that the marine biologist Jeremy Jackson calls “shifting baselines.” But it is hardly normal: it is evidence of loss—of the coastline, the beach—and the public right to the intertidal zone.

In the 1980s, a few prescient coastal scientists, seeing where we were headed, began lobbying legislatures to ban armor. Their first major success was North Carolina where coastal geologists, including Orrin H. Pilkey Jr., of Duke University, led the charge.

Once the ban on armor was in place, storms would annually send one or two unprotected beach houses tumbling into the surf. Pilkey predicted that the first major test of the ban would occur when it threatened its first condo. That test occurred at a complex at the edge of a notoriously unstable inlet in the 1990s. As the price of units fell dramatically, canny buyers purchased units, betting against enforcement of the armor ban. They won their bet, and armor in the form of giant geotextile tubes was put into place. The condo complex survived.

Meanwhile, by the 1980s, it was clear that putting fixed armor on naturally shifting beaches would almost inevitably damage or destroy them, and so a new way was devised to preserve beachfront buildings by artificially replacing their lost sand. “Beach nourishment” involved dredging sand from elsewhere, mixing it into a slurry with seawater, and pumping it onto the depleted beach.

One early project, in Ocean City, Maryland, famously began washing out in 1989, even before the equipment used to build it had been removed. Coastal engineers have refined their work since then, but still the projects erode regularly, so advocates describe them as “sacrificial” dunes and beaches—designed to fail. From this perspective, if the beach vanishes in a storm but the buildings behind it remain, the project is a success.

By the 1980s, it was clear that putting fixed armor on naturally shifting beaches would almost inevitably damage or destroy them, and so a new way was devised to preserve beachfront buildings by artificially replacing their lost sand.

On the whole, beach nourishment is almost always less damaging to the beach than armor, but it comes with unique problems. The projects are noisy and unsightly and usually must be done during tourist season, when the weather is calm. They can also interfere with shorebirds and nesting sea turtles. They require vast quantities of sand that matches the color and grain size of the original beach. By now, close-in sources are increasingly played out, meaning sand dredging and pumping operations get pricier over time. Though costs vary widely, beach nourishment projects typically cost at least a few million dollars a mile.

Under federal law, beaches whose erosion is deemed to result from federal “navigation works” that interfere with sand flow, including jetties at inlets or even groins on a beach, are eligible for up to 100% federal funding. Communities lobby furiously for these fully funded federal projects. And to hedge their bets, they may also establish dedicated taxes, often on tourist-related businesses, to finance the projects.

Once an area of shoreline becomes dependent on renourishment there is no turning back. It will be required indefinitely or the beach—so important for tourism—will disappear. For many coastal towns, beaches have become crucial economic infrastructure requiring regular maintenance.

The third response to the shifting sands has been to raise things up, out of harm’s way. The technique has a long history in Asia, but it did not take hold in the United States in a big way until the flood insurance program required it.

When the insurance program took effect, scientists set elevation requirements in its building codes by looking at topographical maps and estimating the size of the storm surge that a Category 3 hurricane (with winds of 111 to 129 miles per hour) would send ashore if it hit a given locality head on. The codes declared that new construction must be elevated on pilings above that height.

That’s why coastal visitors today see house after house standing on stilts, some of them awkwardly wading in the surf. For many of us they seem normal—another example of how much our baselines have shifted.

Come storms or erosion, residents refuse to leave

Today, all along the coasts, we find wall-to-wall condos, swollen beach shacks, and stilted houses, all fronted either by artificial beaches maintained at enormous expense or walled in by armor. The costs of this 60-year development binge are threefold. First is coastal armor’s degradation or outright destruction of miles of natural beaches. Second is the cost of artificially maintaining miles of beaches. Third is the enormous cost of disaster recovery.

To reduce these costs there is only one way forward: retreat. Few people on the coast like it. Many reject it as downright un-American. But like the people who lived on the coast hundreds or thousands of years ago, we need to get ourselves out of harm’s way.

However, over the past four decades, repeated efforts to pull back from the coast have foundered under opposition from the people who benefitted economically from coastal development and the government policies that support it.

Like the people who lived on the coast hundreds or thousands of years ago, we need to get ourselves out of harm’s way.

In 1982, in a clear, though unspoken, acknowledgement that the flood insurance program had unleashed a demon on the coast, Congress passed the Coastal Barrier Resources Act, which mapped undeveloped areas and identified those that would not be eligible for subsidized flood insurance or disaster aid. Beaches in the zone could be developed, but only “provided that private developers or other non-federal parties bear the full cost.”

Today CBRA covers 2,500 miles of coastline in 23 states and territories. But much of that was never likely to be developed in the first place because it is in national seashores, state or local parks, or other conservation areas.

All too often, people who own buildable land in CBRA zones have simply persuaded their representatives in Congress to push through legislation “correcting” the CBRA maps to exclude their property, as happened, for example, at Cape San Blas, Florida, when a major paper company decided to sell off hundreds of CBRA-protected woodlot acres for development. In other cases, such as on North Topsail Island, on the North Carolina coast, people built and rebuilt, betting (usually successfully) on the reluctance of politicians to turn their backs on them in a disaster—even a disaster they brought on themselves.

In a 2019 study, researchers estimated that CBRA saved the taxpayers $9.5 billion in disaster funding between 1989 and 2013. That sum is substantial, but compare it with the Federal Emergency Management Agency’s estimate of federal insurance payouts for a single storm, Hurricane Sandy in 2012: at least $70 billion in claims. In short, CBRA has not met the high hopes many had for it.

Several states have tried to push development out of harm’s way by establishing setback lines that move inland as dunes and beaches migrate in the face of erosion and rising sea levels. The approach preserves natural features, but often homeowners fight back.

For example, when South Carolina attempted to bar building on sites that had been under water within the past 40 years, the owner of two suddenly unbuildable lots sued on the grounds that he was entitled to compensation for what amounted to a regulatory taking. In 1992, the Supreme Court sided with him. The state bought his lots and then sold them to another builder. By then, South Carolina had already vitiated its setback regulation, because the anticipated flood of litigation would have bankrupted the state.

Similarly, the Texas Open Beaches Law of 1959 provided public access to the beach between the low tide line and the first line of inland vegetation. As waters rose and the vegetation line moved landward, the public access moved with it, and at times, homeowners who found themselves suddenly occupying public trust land were compelled to move their houses.

That changed in 2013 when a Galveston property owner challenged the requirement. The case was settled by the Texas Supreme Court, which ruled that because the landscape changes in question were caused by “an avulsive event” (a storm) rather than the slow progress of erosion, the restrictions did not apply. No one I know claims to understand the logic of that decision. But there is no doubt it significantly weakened the Texas law.

Another attempt at moving development out of harm’s way stalled in the 1990s, when FEMA scientists proposed drawing—and regularly updating—maps delineating areas threatened with serious erosion in the next 10, 30, or 60 years, and limiting construction in high-risk zones. Property owners would have been required to disclose those risks to potential buyers.

Few on the coast wanted this erosion risk data because it could only reduce property values. In 1992, when the plan was subjected to congressional hearings, it perished in a buzz saw of opposition from real estate and building interests. After one hearing, Stephen P. Leatherman, then head of the Coastal Research Laboratory at the University of Maryland, summed things up: “There is a constituency of ignorance on the coast.”

One strategy that has successfully kept development off beaches has been acquiring land for conservation.

Ultimately, one strategy that has successfully kept development off beaches has been acquiring land for conservation. As legislation and technocratic workarounds failed to stop building, people devoted to the conservation of coastal land simply began accelerating efforts to buy coastal land even though it was now about the most expensive anywhere. Predictably, real estate interests from Cape Hatteras, North Carolina, to Gaviota, California, who hate to see a good development opportunity slip away, have battled local and national attempts to conserve seashore.

Where I live—Chappaquiddick Island, which hangs off the east end of Martha’s Vineyard—all the beaches are protected either because they are county open space or because conservation-minded fishers and others led the effort to purchase the rest, according to local lore. Now all of Chappy’s beaches are managed by The Trustees of Reservations, a Massachusetts conservation organization, and except for a few in-holdings they are unbuilt.

Hurricane Sandy clobbers an attempt at reform

Finally, in 2012, Congress passed the Biggert-Waters Flood Insurance Reform Act, which, among other things, called for substantial increases in flood insurance premiums and limits on repeat claims. When I heard it had passed I experienced a frisson of hope that at last something sensible was being done. Almost immediately, however, I realized that if push really came to shove, it was unlikely the new provisions would survive.

That “shove” came on October 29, 2012, when Hurricane Sandy traveled up the East Coast to Brigantine, New Jersey, where it collided with another low pressure storm system and made landfall. The result was a “superstorm” with surges of seawater of up to 10 feet or more.

The widespread damage provoked some people to suggest that there were parts of the region’s coast that were too dangerous to be rebuilt. There was talk of turning certain flooded areas into open spaces or parks. But soon, that kind of talk was replaced with public service television ads featuring Robert de Niro and Al Pacino and other local celebrities promising the region would build back, bigger and better than ever.

As that process got underway, property owners fought the realities of Biggert-Waters, encouraging Congress to weaken, delay, or otherwise undo the law—which it did in the Homeowner Flood Insurance Affordability Act of 2014.

Another attempt to undo the harms and costs of the insurance had largely failed, but sea levels still continue to rise. In 2010 a panel of coastal scientists charged with offering guidance to North Carolina policy-makers reported to the legislature that their models predicted sea levels could rise by 39 inches by 2100. That would be devastating on the state’s coast, where barrier islands are mostly narrow and low-lying, where the population has grown by half since 2000, and where businesses produce most of the state’s tourism income.

The legislature rejected the report, passing a bill in 2012 instructing policy-makers to assume that sea levels would rise in the twenty-first century no more than they had in the twentieth—just under one foot. Though the action was later modified to include a review in a few decades, it made the legislature an international joke.

And it did nothing to stop the sea’s assault on the state’s beaches and coastal infrastructure. NC12, the main road along the Outer Banks, requires massive rebuilding on an almost yearly basis. Fortunately, as one public works official told me, crews have so much experience by now they can do the job quickly.

Could we give the beach back to the turtles?

Where do we go from here? An adage of economics has it that if a thing cannot go on forever, eventually it will stop.

For too long coastal communities have bet everything on a combination of federal largesse and engineering know-how that was never sustainable. Now, with sea level rise, it is becoming physically and economically impossible.

Already, coastal communities regularly experience so-called sunny day flooding when the moon is full and the tide is high. Soon many streets in places such as Miami, Charleston, South Carolina, and Norfolk, Virginia will be more or less permanently flooded. Norfolk has already begun raising its streets.

America’s biggest coastal mistake was creating federal subsidies that enabled developers to escape the realities of nature and the market. Can we undo that? Suppose we abandoned the federal insurance program and simply allowed market forces to shape development on the coast while allowing the forces of the ocean to shape the coast itself? What would that look like?

America’s biggest coastal mistake was creating federal subsidies that enabled developers to escape the realities of nature and the market. Can we undo that?

Already, some market forces are starting to intrude on the real estate market on the coast. For example, advertisements that once might have emphasized easy beach access now talk about the high elevation of their lots and websites such as Zillow inform would-be buyers about properties’ flood zones.

Suppose we were able to limit flood insurance payouts by, say, informing policyholders they could make one more claim and after that their property would be barred from subsidy? Over time that would at least reduce the program’s expenses and might discourage rebuilding in places obviously unsuited for it.

Or suppose we were to take more seriously the public’s Common Law right to traverse “the shores of the sea,” the intertidal zone of the wet beach. Suppose that when the installation of armor leads to the drowning of that beach, or the wet beach gradually migrates under a house on stilts, the legal system responded to what really amounts to a private taking of public land? If people had to pay for taking that land, they might think twice before building near it. What would that look like?

It might look a lot like Chappaquiddick.

As I write, Hurricane Isiasis is wearing itself out in northern New England somewhere, after treating us to days of heavy wind (but no rain). The Trustees have just posted an update on beach conditions, and the news is bad. Wind-driven water has produced severe erosion and washed out the overland vehicle trails. Vehicle access to Wasque Point, a prime fishing spot, is closed.

But when the weather calms, sand will start to move back onto the beach—we can already see it sitting offshore in shoals where waves break at low tide. Rangers will survey the damage and see where a new trail might be set up. No buildings will have fallen into the ocean, because there are hardly any to fall on that shifting, eroding, and ever-beautiful beach.